What will be the effects of the European Union’s CBAM (Carbon Border Adjustment Mechanism) in the Mediterranean? Hard to predict today.

The CBAM will take effect from 2026 with a transitional phase. The mechanism will gradually impose a proportional tax on emissions of emission-intensive products such as aluminum, hydrogen, cement, electricity, fertilizer, and steel imported from third countries to the EU. This tax will be calibrated to equalize product costs among European producers, who are subject to carbon pricing mechanisms (EU ETS[1] ) that affect the final cost of production, versus non-EU producers, for whom there are no such regulatory restrictions with respect to GHG emissions in production processes.

This mechanism was designed to rebalance the risk of relocation of production to countries without emission constraints and, at the same time, steer demand toward ‘greener’ products. However, in the absence of mechanisms to encourage investment in ‘cleaner’ and more sustainable technologies and production processes, it could only result in a ‘barrier’ to access and economic development for Europe’s trading partners and an increase in the final cost of goods for European producers. Such an effect could isolate Europe and hinder the industrial transformation necessary for climate goals to be effectively achieved globally, not just in Europe. It is necessary, therefore, to take these consequences into account especially with respect to the ‘closest’ trading partners, such as those in North Africa, also in relation to the interconnectedness of value chains on a global scale.

Beyond the significant trade in petroleum products and gas[2] , France, Italy and Spain are among the top trade destinations for manufacturing in North African countries.

Looking at manufacturing sectors, the extent of trade between North Africa and Europe is shown in the figure below.

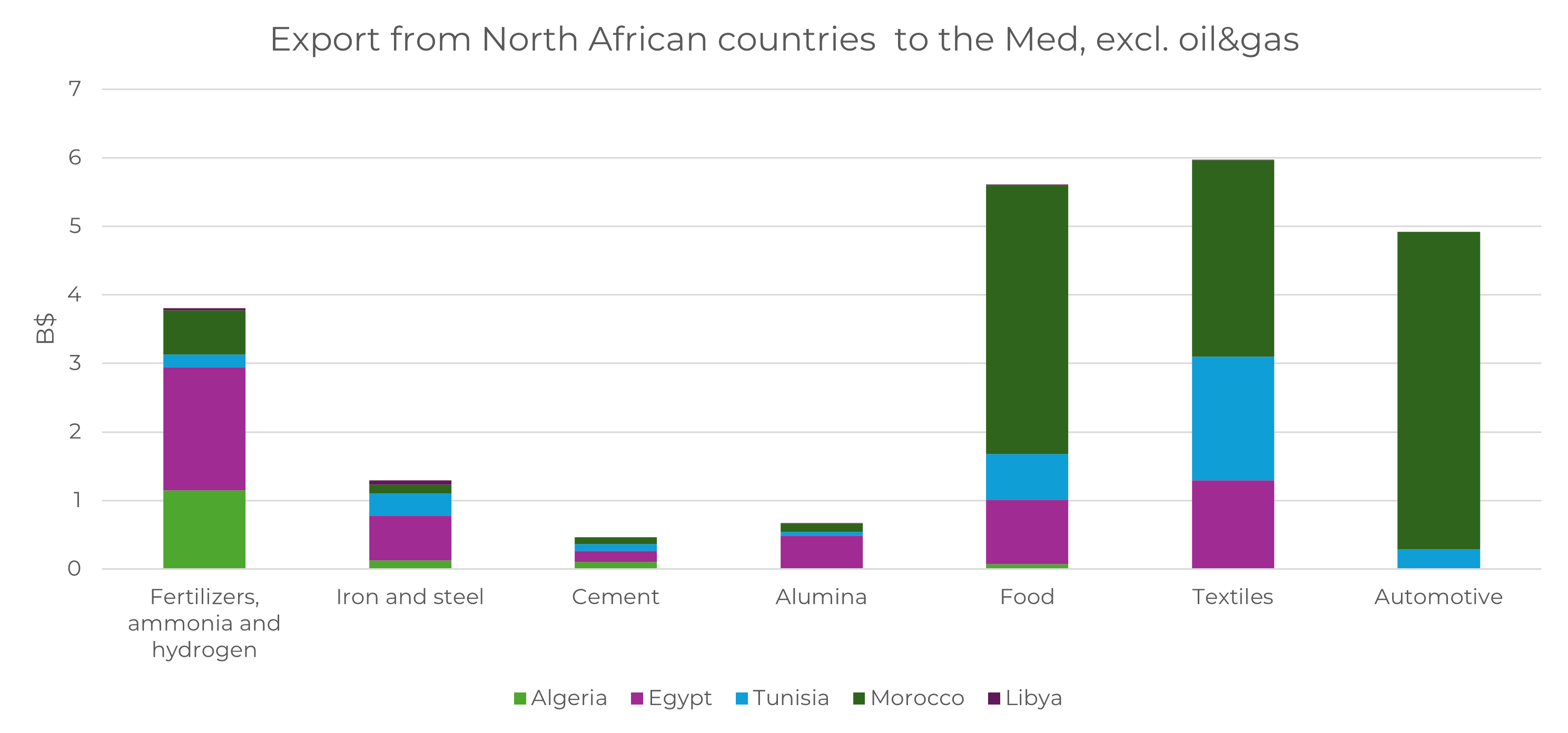

Manufacturing exports from North African countries to the northern shore of the Mediterranean [3]

Fertilizers and inorganic chemicals, including ammonia and hydrogen, reached $3.8 billion[4] . In this sector, Egypt exported 47 percent of the value, followed by Algeria with 30 percent. The steel sector reached about $1.3 billion, with Egypt exporting 50 percent and Tunisia 25 percent. Finally, aluminum and cement, ~$0.7 billion and ~$0.5 billion respectively, saw Egypt’s share of 74% and 34%.

Looking at the sectors not included in the CBAM but, nevertheless, subject or to be subject to the EU ETS from 2026 onward, the automotive sector (cars, tractors, trucks, and spare parts) reached about $5 billion, with Morocco standing out among the producing and exporting countries (94 percent). Furthermore, in 2022, the textile sector reached about $6 billion and sees a significant share of Morocco (48 percent), followed by Tunisia (30 percent) and Egypt (21 percent). Food exports reached $5.6 billion, with Morocco exporting 70 percent of the total value.

The main exports from France, Italy and Spain to North Africa, however, include cereals (France traded about $2.5 billion with Morocco and Algeria), machinery, mechanical equipment and related components.

From the data, the CBAM will affect the economies of North African countries in very different ways. By applying a carbon price to the above products, it will make these products more expensive for EU importers and likely less competitive with low-carbon alternatives unless current exporters put in place measures to decarbonize these productions or carbon pricing measures equivalent to those in Europe.

Among the Mediterranean countries, Algeria is perhaps the one most likely to be affected, which, incidentally, could affect Italy more closely than other European countries. After gas, in fact, the country exports to the EU mainly fertilizers, ammonia and hydrogen[5] , where it has more than 140 companies operating, as well as steel (where it has 7 main companies employing more than 3,000 workers), cement (where it employs 12,000 workers) and alumina[6] . These are all products that fall within the CBAM and for which Italy depends on foreign imports with price repercussions.

Countries such as Egypt, with a more diversified and integrated economy[7] or such as Morocco and Tunisia, may be less impacted as they specialize in different sectors, such as automotive manufacturing, food and beverages, and textiles. However, a future extension of mechanisms such as CBAM on other sectors cannot be ruled out, so assessing the effects of such a rule, both with respect to the immediate trade and cost impacts and on the actual contribution toward combating climate change is a necessary step.

The CBAM, in its current design, seems to have more the traits of a protectionist measure than a lever to promote industrial transformation in line with decarbonization in Europe and North African countries. North African countries, as things stand, may in fact have less access to the technologies and investments needed for decarbonization, and thus find it difficult to adapt quickly. Likewise, European producers would see increases in production costs with competitive repercussions, particularly for export-intensive countries such as Italy. For this reason, the implementation of the CBAM in a framework of regional cooperation and support that may also include the application of harmonization measures such as CO2 pricing mechanisms equivalent to the EU ETS should become a priority of the new EU Commission.

The Mediterranean area lends itself well to being a laboratory for new collaboration mechanisms for economic development based on reciprocity and synergy of action among the countries in the area. The Commission’s new mandate puts at the center of its action the challenge of Europe’s competitiveness in the perspective of decarbonization and adopts, for the first time, a privileged look towards the Mediterranean area with the appointment of a dedicated Commissioner. There is, therefore, an opportunity in assessing the consequences of unilateral mechanisms such as the CBAM and, potentially, modifying them to make them more effective toward achieving climate goals, not only in Europe, but by accelerating investment in ‘cleaner’ technologies in third countries as well.

–

[1] Emission Trading Scheme defined by European Directive 2003/87/EC

[2] In 2022, Algeria, Egypt and Libya traded about $50 billion worth of oil products and gas[2] . Italy re-exported about $3 billion worth of refined products to North African countries and Spain $1.8 billion.

[3] Values represent trade between the 5 North African countries and Italy, France, Spain, Greece and Turkey

[4] Economic values are always referred to 2022.

[5] It should be noted that hydrogen and ammonia are part of the value chain of fertilizers themselves.

[6] Data provided by the pan-Arab research center RCREEE in Cairo (Regional Center for Renewable Energy and Energy Efficiency).

[7] In fact, the country has 9 major companies in the steel sector, more than 9,000 chemical companies and more than 17,000 companies in the non-ferrous metals sector – Data provided by the UNIDO (United Nations Industrial Development Organization) office in Cairo